When really getting ready to buy a home, your Financial Advisor or Loan Officer will evaluate your current financial picture to see if you are in a position to take on a mortgage. Buying a home is a very emotional experience, and I want you to be practical first and financially secure so when you do find that home you are financially ready. The general rule of thumb is to spend 28% or less of your monthly gross income (e.g. principal, interest, taxes and insurance) on your mortgage payment. To determine how much you can afford using this rule, multiply your monthly gross income by 28%. For example, if you make $10,000 a month then multiply $10,000 X .28 to get $2800. Using this method your monthly mortgage payment should be no more than $2800. The second thing you need to understand is your debt-to-income ratio. While your gross income is step 1 in figuring out what you can afford, knowing your DTI ratio is step 2. Simply put, your DTI is how much you make versus how much debt you have. Lenders use both your gross income and DTI to determine how much you can afford and therefor how much they will lend. To understand your DTI, take all your debt such as credit cards, car payment, student loans, etc. and divide it by your gross monthly income. Next multiply that number by 100. You want a low number. So if you make $10,000 a month and you have $2500 of monthly payments you would take $2500/$10000 X 100 or 25. This is a low DTI number and you can see that if you make $10,000 and your mortgage from above was $2800 and you DTI is $2500 you have $4700 left per month for entertainment, savings, food etc. Having this basic understanding of your financial picture will help you make educated decisions on what you can and cannot afford. With all this said, I recently convinced two buyers to wait a year and pay down some of their debt before buying a home. This is not always the thing someone wants to hear when they emotionally want to buy a home. Practically, they both agreed it was the smart decision.

Like them. If you have debt, you’re not alone. The average American is over $80,000 in debt, excluding home mortgages. But unexpected or unplanned debt such as medical bills or credit card balances can be a tipping point into financial insecurity. You have too many payments every month, you might get behind on other financial goals such as building an emergency fund, taking a vacation, or adding to a retirement account.

Here are a few tips for reducing your debt.

Before you start paying off debt, tally how much debt you have. Make a list with this information for each bill you owe.

The details you need to know about every debt:

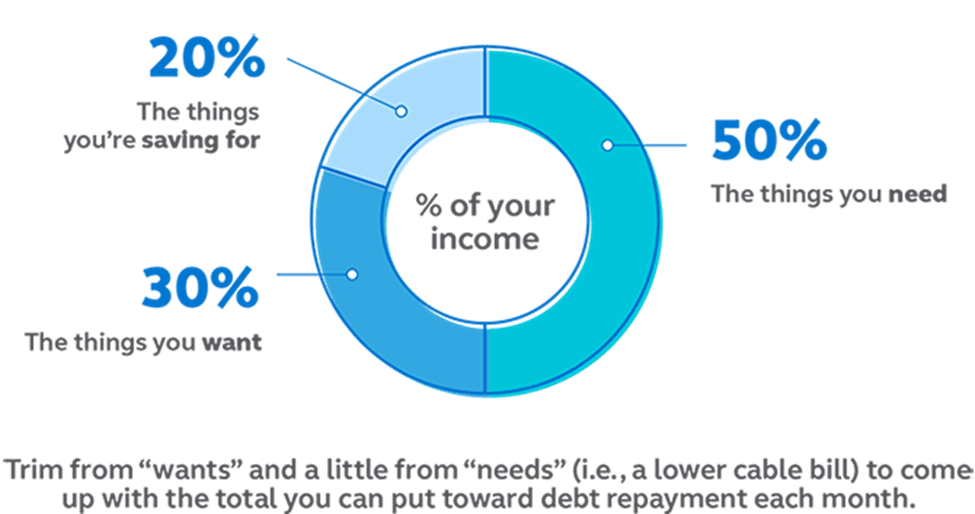

The 50/30/20 approach[2] simplifies budgeting:

4. Pick a debt repayment strategy.

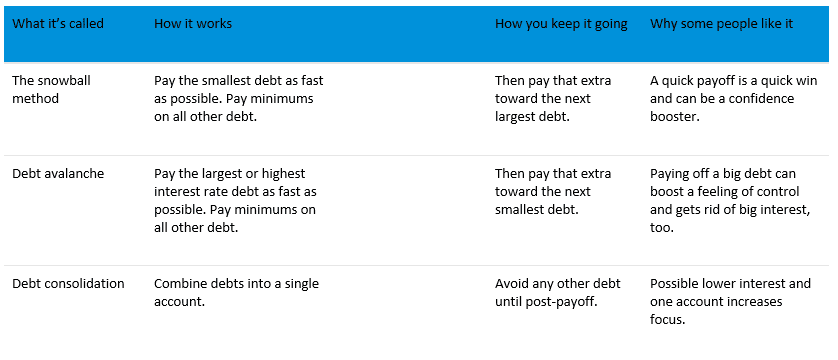

In general, there are three debt repayment strategies that can help people pay down or pay off debt more efficiently.

The Debt Snowball

The debt snowball method builds momentum as you start repaying creditors, like rolling a snowball across the ground. Begin by paying off debts from smallest to largest. List debts by balance and start with the smallest one. Make sure to pay minimums on all other bills and send extra cash to the debt with the smallest balance until it’s paid in full.

Repeat this strategy with the other debts. As you pay off balances, you’ll free up more funds for other debts. Plus, it’s encouraging to see progress and can keep you on track to see debts vanishing.

Who this is best for: The debt snowball is best if you want to experience quick gains when paying off your debts.

The Debt Avalanche

The debt avalanche strategy takes a similar approach but instead orders debts by interest rate. First, you make a list of all your debts from the highest interest rate to the lowest. You then concentrate on paying off the highest-interest debt first while making minimum payments on all the other debt. This cuts back on the amount you’re paying in interest, which also frees up more cash to pay down other debt.

Who this is best for: The debt avalanche is suitable if saving a bundle in interest is a priority, and you’re motivated to get out of debt quickly.

Debt Consolidation

If it becomes too challenging to keep up with various payments and due dates, consider debt consolidation. A personal loan or a new balance-transfer credit card could be used for this purpose. With debt consolidation, the lender pays off all your existing debts and rolls them into one new loan with one payment. While the new interest rate may be higher than some of your other bills, you could wind up saving money by avoiding missed and late payment fees.

To determine if it’s a smart strategy for your situation, you’ll need to calculate your blended interest rate. It’s the combined interest rate paid on all your debts. It’s calculated by summing the total interest you’ll pay in a year and dividing it by the entire principal owed.

Even though the rate on a debt consolidation loan can be quite high, it could still be lower than the blended rate you’re already paying, in which case a debt consolidation loan would be a good choice. Who this is best for: Consider debt consolidation if you can commit to not using your credit cards or acquiring more debt while you work to pay off what you owe.

E3 Home Loans CA

Published on December 12, 2022

Compass

16268 Los Gatos Blvd.

Los Gatos, CA 95032

CA DRE# 01955771

Susan Ward