Compass is fortunate to have a fantastic internal market analyst, Patrick Carlisle that provides us with market data sliced and diced in every possible scenario. Read on to better understand the current market and how it compares to previous real estate environments. In this very tentative time, facts must always prevail, and it will calm you down!

Even the hottest markets eventually cool. This does not necessarily imply a large “bubble and crash” (terms much overused). Over the past 4 decades, a cooling shift has typically meant a gradual decline in sales activity, then either a leveling off in appreciation or price declines of 5% to 10%: More like a slow leak in an over-pressurized tire than a blowout at high speed. The 2008 subprime crisis – a true bubble & crash – was an extreme event brought about by a massive failure of ethics, underwriting standards and risk management in the loan, banking, investment and ratings industries.

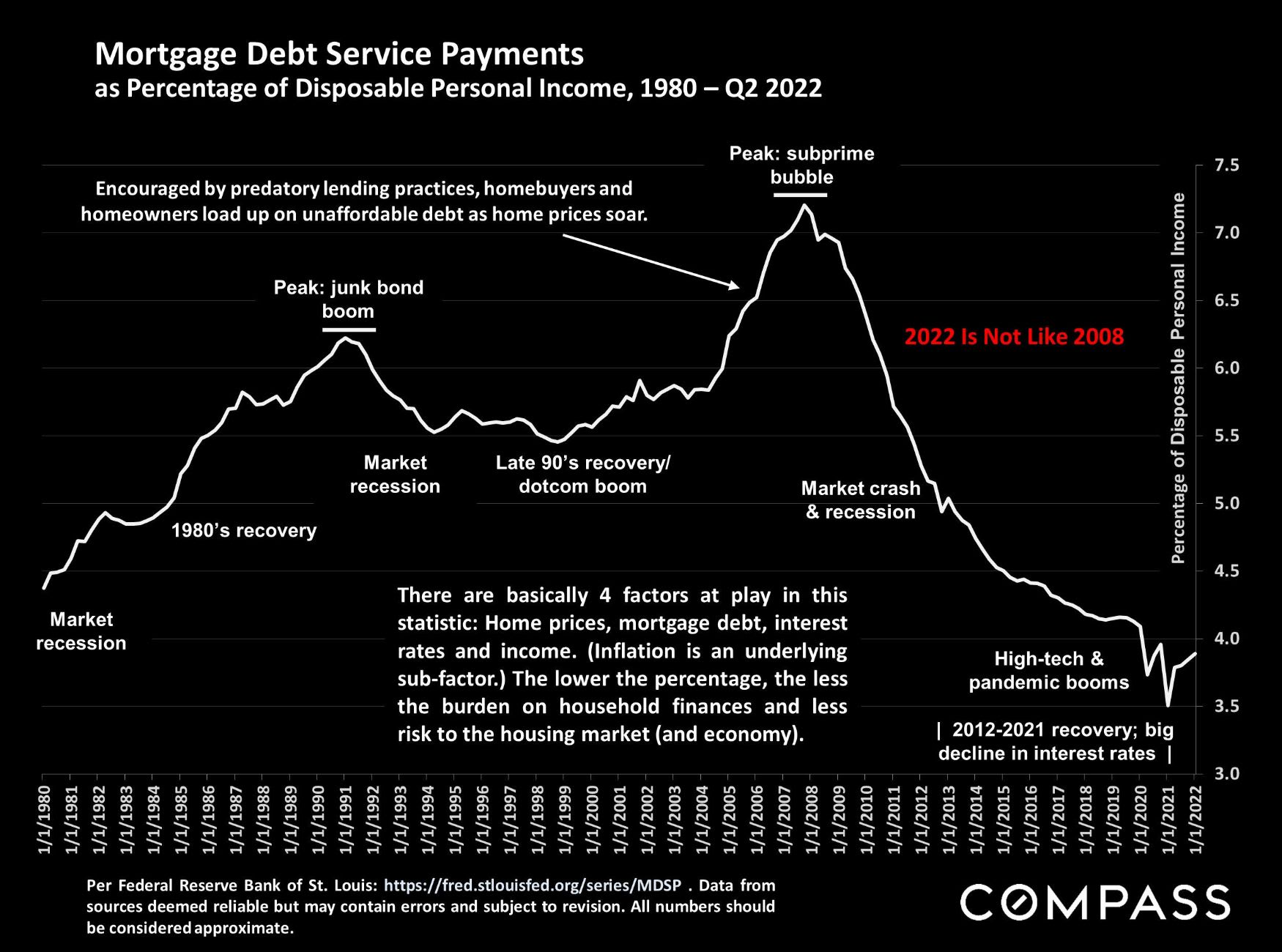

A correction is not a crash. The precipitating factor in the 2008 crash – tens of millions of households talked into home loans they couldn’t afford, forcing frantic sales during a recession – does not apply today. Indeed, mortgage payments as a percentage of income are close to all-time lows (and most homeowners’ mortgages are also at historically low rates). Outside the 2008 crash, market corrections over the last 4 decades typically ran from a simple flattening in appreciation, to price adjustments of 5% to 10% (relatively small compared to the appreciation rates which preceded them).

Staggering levels of unaffordable mortgage debt was a huge factor in the 2008 crash, but right now, mortgage debt as a percentage of disposable income is close to an all-time low. A tsunami of foreclosures and short sales - behind the home price crash in 2008-2011 - is not imminent:

This is a quote used in its entirety by the SF Chronicle in July:

The 2008 collapse “was an anomaly,” Carlisle said. “The 2005-2007 bubble was fueled by home buying and refinancing with unaffordable amounts of debt on a staggering level, promoted by predatory lending practices, promises of endless appreciation, and an abysmal decline in underwriting standards — and then eagerly facilitated by smug, rapacious, Wall Street flimflammery and self-abasing credit ratings agencies,” he wrote in a report last year. “Millions came to own homes they could never afford to pay for and the rot was distributed throughout the financial system.”

Compass

16268 Los Gatos Blvd.

Los Gatos, CA 95032

CA DRE# 01955771

Susan Ward