Are You Ready to Buy a Home?When I speak to first-time home buyers, more times than not, we decide that they might need another 6-12 months to truly be ready to buy a home. I would much rather you wait and get financially secure than jump into homeownership because of a great deal. There will always be another great deal. Determining how much money you need to buy a house has always been daunting for first-time homebuyers, but 2023 may feel like a new level of frustration. While it remains a seller’s market in most areas, buying a home is still a smart move that can help you lay a strong financial foundation for your future. Here is a rundown of the key costs to making homeownership a reality.

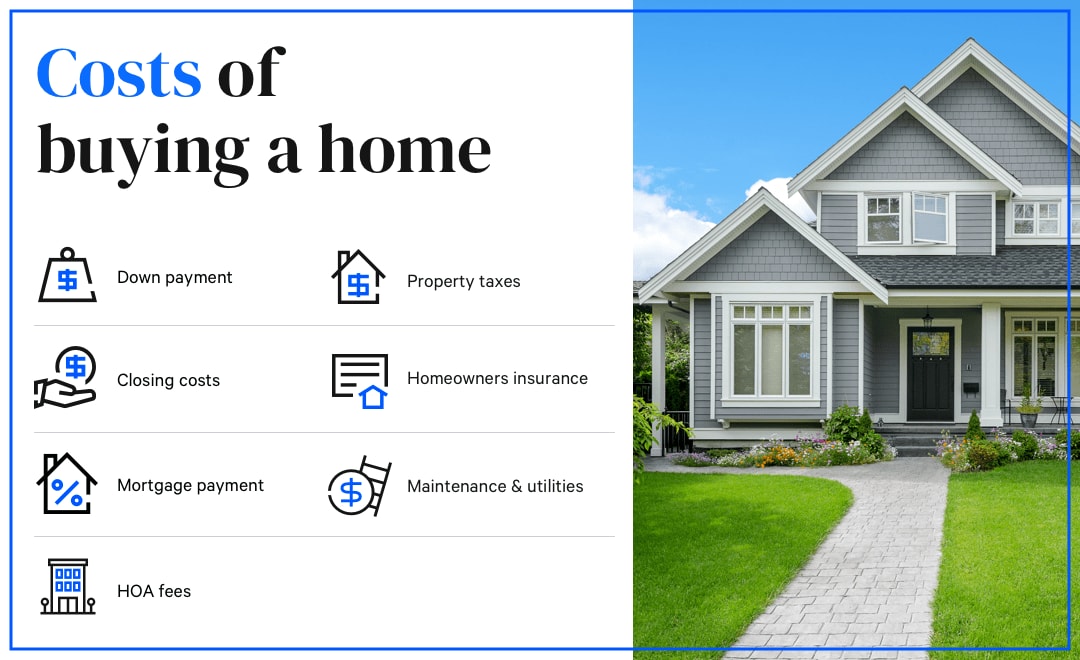

Breaking down the cost of buying a home

Breaking down the cost of buying a home

As you consider the price tag of a home, it’s important to calculate the major expenses you’ll need to cover in order to call it your own:

1. Down payment

The down payment is the amount of money you contribute to the home purchase upfront. By increasing the size of your down payment, you can lower the amount of money you need to borrow — which, in turn, lowers your monthly payments over the course of the loan. Lenders like to see larger down payments because they indicate a lower level of risk if you default on the loan.

How much should you put down on a house?

There is a common misconception that you need to put down 20 percent of the purchase price. (If you’re buying a home that costs $400,000, a 20 percent down payment would be $80,000.) In fact, first-quarter 2023 data from Realtor.com that the average down payment on a primary residence was just 13 percent.

In addition, several low and no closing cost options allow for even less money upfront. Some conventional mortgage programs backed by Fannie Mae and Freddie Mac require just 3 percent down. The caveat with these types of loans is that they can have income restrictions and require a higher credit score. FHA loans require just 3.5 percent down, and you’ll need a credit score of at least 580 to qualify. VA loans and USDA loans don’t require a down payment at all, although you’ll need to meet certain criteria to be eligible.

Ultimately, figuring out your down payment means thinking about the rest of your budget. You shouldn’t spend every penny you have to cover your down payment — you’ll stretch yourself too thin and stress yourself out as you try to cover all your other necessary expenses. Plus, a lender will evaluate your entire financial portfolio and want to see some cash reserves that you can use to pay back your loan if you find yourself in a tough spot. And you should also make sure you have enough set aside in an emergency fund to provide a cushion if you receive an unexpectedly large medical bill, lose your job or find yourself in any other worst-case scenario.

Tips to build your down payment fund

Regardless of how much you plan to put down when you buy a home, coming up with that big upfront cost requires some work. Consider these helpful tips to build your down payment funds.

- Look for local support: Browse first-time homebuyer programs in the city and state where you want to buy. Some offer grants or zero-interest loans for your down payment costs, if you qualify.

- Identify every expense you can cut: Saving more starts with spending less. Can you cancel your cable? Are you overpaying for your cell phone service? Should you be dining out less? Look at your weekly and monthly expenses to find ways to trim your spending.

- Put your savings to work: From CDs to high-yield savings accounts, every extra penny counts. Rather than saving in an account that pays little to no interest, compare interest rates on options where you can park your money. Just be sure you’ll have access to the funds when you need them.

- Ask for help: If you have a relative or close friend who has the money — and loves you enough to give it to you with no strings attached — a gift can be used for the down payment. A lender will want reassurance that it is, in fact, a gift and not a loan, so plan to submit a gift letter that explains you won’t need to pay it back.

2. Closing costs

The down payment isn’t the only upfront expense you need to consider. You can expect to pay 2 percent to 5 percent of your mortgage loan principal in closing costs. In 2021, borrowers paid an average $6,905 in closing costs and taxes on a single-family home, according to ClosingCorp. Closing costs vary widely based on where you’re buying, however. For example, average closing costs in Washington, D.C., were nearly $30,000, but they were just $2,061 in Missouri.

What is included in closing costs?

Closing costs include a range of fees charged by your lender and other companies involved in approving your loan and finalizing the sale. These can include fees for the following:

- Appraisal

- Credit report

- Origination

- Application

- Title search

- Title insurance

- Underwriting

Closing costs vary from lender to lender, so pay close attention to the origination fee and underwriting fee to see where you might be able to save. It’s important to note that you’ll likely pay some additional expenses on closing day that aren’t considered closing costs. These are known as prepaids, and can include homeowners insurance premiums and property taxes. You’ll also prepay interest on any days remaining through the end of the month. For example, if you close on April 20, you will prepay on interest through April 30.

Can you avoid closing costs?

You can’t avoid closing costs completely, but you can avoid paying them all at once. You may also be able to negotiate at least some closing costs, especially in a buyer’s market.

If coming up with cash to pay for closing costs seems daunting, ask your lender about no closing cost options. Some lenders will roll the expenses into the overall loan. Just keep in mind that doing so will cost you more in the long run, since you’ll be paying interest on the additional amount.

And on top of closing costs and prepaids, you’ll also want to earmark money for moving expenses, furniture, repairs, storage or any other costs you will encounter as you move into your new home.

3. Prepaid costs

Apart from closing costs, you’ll also need to pay prepaid costs. These are upfront cash payments that you make at closing for certain mortgage expenses before they’re actually due, including things like homeowners insurance, property taxes and mortgage interest. For these monthly recurring expenses, your lender will likely hold your funds in escrow until the bills come due.

Earnest money

Prospective buyers also pay an earnest money deposit to demonstrate serious intent to purchase a home. You’ll typically need to pay 1 percent of the home’s agreed-upon purchase price. But earnest money is not an additional expense, it’s just paying a bit of your expenses early. You make the deposit within a day or two after your offer is accepted, and at closing, it is credited toward your payment.

Cash reserves

Your lender will also want to see that you have enough remaining financial reserves to cover your mortgage payments in the event of an emergency or change in income. Mortgage reserves are measured in months. For example, if you have $7,200 in a savings account after closing on your house, and your monthly home loan payment is $1,200, you have six months of reserves. Non-liquid assets, like funds that can only be withdrawn upon retirement, typically don’t qualify as reserves.

4. Moving costs

In addition to actually buying a home, you need to budget for the costs of moving into it. Prices vary based on the size of your home, the distance you’re moving, the weight of your items and whether you’ll need storage for a time in-between. According to Home Advisor, a typical move ranges between $913 and $2,528, with the average being about $1,711.

Be sure to factor in the costs of small expenses that add up in aggregate, such as boxes, packing tape, and bubble wrap. You should also consider the potential cost of changing your address on various accounts and IDs, and look into how bills like auto insurance might change with a new address as well.

Local vs. out of state

Keep in mind that, while local moves might be expensive, out-of-state or cross-country moves are much costlier. Long-distance moves also incur additional expenses along the way, such as the cost of lodging, gas or airfare as you move from Point A to Point B.

5. House payments

As you’re thinking about how much money you need to buy a house, it’s crucial to know how much it will cost you every month, not just on closing day.

Your monthly mortgage payment is one of the most predictable ongoing costs. You can use Bankrate’s mortgage calculator to figure out how much you’ll owe each month. For example, if you borrow $240,000 and finance it with a 30-year, fixed-rate mortgage at 6.0 percent, you’d pay $1,438 in monthly principal and interest.

How can I get the most affordable house payment?

Your mortgage rate has a big impact on your monthly mortgage payment, which makes it crucial to shop with multiple lenders for the best mortgage rate. For example, if you got that same $240,000 loan at a 7.0 percent rate, the payment for monthly principal and interest increases to $1,596.

According to a Consumer Financial Protection Bureau, more than three-quarters of all borrowers only applied for a mortgage with one lender. Failing to comparison-shop could cost you thousands over the life of the loan.

What is mortgage insurance?

In addition to paying the principal and interest, your mortgage payment will likely include mortgage insurance if you put less than 20 percent down. Mortgage insurance is a protection for the lender in case you ever cannot pay the loan back.

If you have an FHA loan, you will almost certainly pay mortgage insurance, which includes a premium upfront and additional premiums built into your mortgage payment. The annual premiums will likely last for the entire loan. If you have a conventional loan with a down payment less than 20 percent, you’ll pay private mortgage insurance (PMI) until you have built up 20 percent equity in the home — at which point you can cancel the PMI. The cost of PMI varies based on your credit and your loan, so be sure to ask your lender for an estimate of how much it adds to your bill.

6. Ongoing homeownership costs

Besides your monthly house payment, you’ll need to account for the ongoing costs of homeownership. Consider budgeting for emergency home repairs and maintenance in the amount of 1 percent or more of your home’s value every year. For example, on a $300,000 home, your budget for maintenance-related items would be $3,000 annually.

Be sure to also factor in homeowners insurance, property taxes, HOA fees (if your property is part of an association), utility bills and regular maintenance expenses.

Preparing to buy a home

Once you’ve answered the big question of how much money you need to buy a house, it’s time to answer another one: how to get ready to make the actual purchase. Here are some steps to take to prepare to buy a home.

- Check your credit: Mortgage lenders use your credit score, along with other criteria, to determine your creditworthiness. You can get your credit score from each of the three major credit reporting agencies, an online service or your bank. If your score is on the lower side, try to take steps to improve your credit before seeking out a mortgage.

- Create a budget: Take a look at all your expenses to create a realistic budget. Many experts recommend following the 28/36 percent rule, in which you should spend no more than 28 percent of your gross monthly income on housing and no more than 36 percent total on debt.

- Save for a down payment: You’ll typically need at least 3 percent of the purchase price of the home as a down payment. Keep in mind that to avoid having to pay for mortgage insurance, though, you’ll likely need to put at least 20 percent down.

- Shop for a lender: Getting preapproved by a lender for a mortgage makes you a more serious potential buyer to sellers and provides you with a better idea of how much home you can truly afford. Start by shopping around and getting quotes from at least three lenders.

- Be willing to compromise: With home prices on the rise, you may need to give up on amenities like a garage or a finished basement as a must-have. Remember that once you own the property, you can always work to make improvements and upgrades in the future.

Next steps

When shopping for a home, it’s invaluable to work with a local real estate agent who knows your market well. Ask family and friends for referrals, and interview several professionals before choosing the Realtor who’s right for you.

You should also shop around and compare rate offers from at least three different lenders before moving forward. Snagging a lower rate upfront can save you thousands in the long run.

Finally, make sure to account for both upfront and ongoing expenses when creating a budget, and take a close look at your monthly finances to make sure that carrying a mortgage and paying for continuing expenses won’t be a financial burden long term.