What’s Different About Today’s Housing Market vs 2008

While there have been comparisons between the Great Recession of 2008 and today's economy, there are actually many significant differences.

The COVID-19 pandemic has had a large effect on the economy – so much so that you might have heard talks of our country entering another recession.

Due to the severity of the 2008 financial crisis and severity of the ensuing recession, the term “recession” stirs up a lot of emotions for many, especially when it comes to the real estate market.

What Happened to the Housing Market in 2008?

The housing market was booming in the early 2000s. Wall Street firms bolstered this growth with demand from an expanding private label residential securities market. To feed this increasing demand, and as house prices continued to increase, many lenders approved subprime mortgage loans for homebuyers with little to no qualifications.

When many of these homeowners inevitably couldn't afford their mortgage payments, mortgage defaults rose substantially, and investors and banks couldn't afford to bail everyone out. This caused a ripple effect in our economy. Enter: The Great Recession.

How is the Current Housing Market Different?

Higher Standards for Loan Qualification

First and foremost, the standards for getting a home loan are far more comprehensive than they were in the early 2000s. The approval process is more thorough, and the guidelines tend to be firmer.

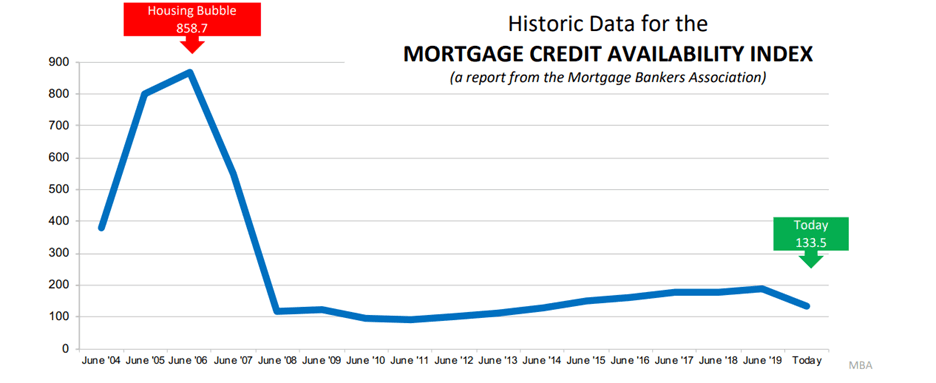

As you can see in the Mortgage Bankers’ Association “Mortgage Credit Availability Index,” home loans were available to just about anyone. Today, the amount of mortgage credit available (in layman’s terms: the amount of home loans given out) is still at a safe, normal level.

Source: MBA

Now, that’s not to say it’s necessarily “harder” to get a mortgage these days. This is something we take pride in here at Waterstone Mortgage – we offer a wide variety of home loan options to suit each homebuyer’s unique situation. At the same time, you can trust that we’re taking the proper precautions to protect our customers and ourselves.

The long-term relationships we have with investors and the proven loan performance track record of our customers demonstrate that Waterstone Mortgage has the best interests of the customer in mind. We strive to only offer loans that our customers will be able to handle, preventing any damage to their future financial health.

Waterstone Mortgage is backed by a bank with $1.9 billion in assets, ensuring financial security for all parties involved. This strong backing allows Waterstone Mortgage to bring more options to customers and to invest in technology that provides customers a better lending experience.

Less Housing Inventory

One of the key factors that caused the burst of the housing bubble was that there was a surplus in inventory. There were more homes for sale than there were buyers, so sellers, some lenders, and real estate investors were far less “picky” about who the home was sold to.

As anyone trying to buy a house right now knows, there is actually an undersupply of homes on the market these days. Because of the higher amount of competition, it’s important to have a pre-approval from a reputable mortgage lender if you’re making an offer on a house. Why? Sellers are more likely to accept an offer that they know won’t fall through. Not only does this extra precaution benefit the seller, but it helps ensure the stability of the housing market too.

Stable House Price Appreciation

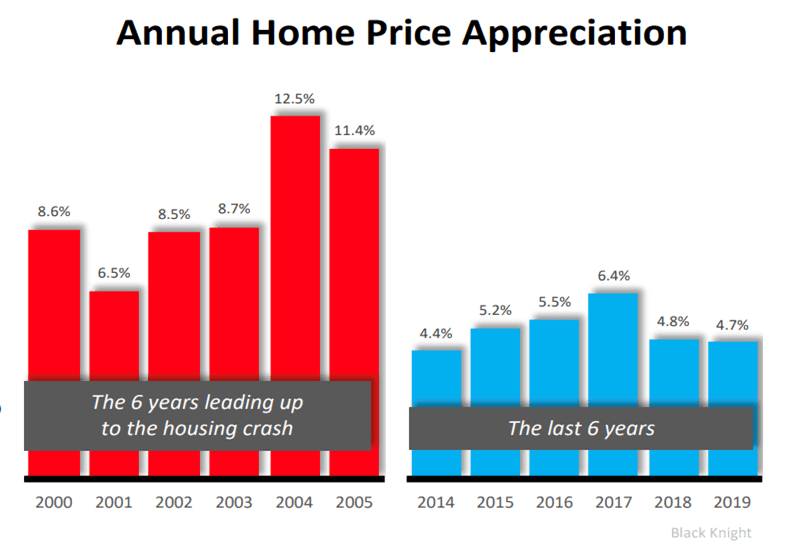

In the years leading up to the housing market crash, home price appreciation (the increase in value of houses) was out of control. They simply became too expensive for buyers to afford, which became another contributing factor to the crash.

The price of homes is still high today, but it’s risen at a far more stable level.

Source: Black Knight

Use of Home Equity

Prior to the housing crisis, many homeowners were using cash-out refinances to supplement their cash flow, meaning they were tapping into their home’s equity as soon as it built up enough rather than letting it grow and build their overall wealth. It became common to hear homeowners were using their homes like an ATM machine.

Source: Freddie Mac

This put many homeowners in a negative equity position when the housing bubble burst; they owed more on their home than it was actually worth.

Should I Buy a House Now?

Unlike the early 2000s, now is actually a great time to buy. The COVID-19 pandemic has certainly shaken things up a bit, but interest rates are still extremely low. Plus, there are plenty of ways Realtors are

keeping the homebuying process safe, like utilizing digital tools, taking sanitation precautions, and more. Lending standards and market conditions are much more stable now.

If you’re ready to start your journey to homeownership,

contact a local home loan professional in your area to learn how to get pre-approved. Contact me for local professionals that I work with on a regular basis.

Waterstone Mortgage by Bob Selingo